“Sports podcasts perform” is one of those things the industry says without ever showing the work. On May 13 at 2 PM ET, Bryan Goldmark from Locked On and Tom Webster are going to show the work — the attention numbers, the trust numbers, and the actual brand campaigns those numbers translated into. Register here.

Before I get going: this piece is longer than the typical Sounds Profitable newsletter, and I want to acknowledge that up front. I’m not a hot, spicy take person. Those I save for the dinner table. MUY CALIENTE. What I try to do in this newsletter is sit down with the actual facts, look at what they say, and show my work. The rumored SiriusXM/iHeart deal seemed like the kind of story that benefits from that approach more than from a fast reaction, so I’m going to take some time today and ask you to come along with me.

If you’re the kind of reader who works through this newsletter on their phone in the bathroom, this one may be a two-tripper if you don’t have sufficient fiber and water intake.

The Deal, So Far

On April 24, Bloomberg Law reported that iHeartMedia and SiriusXM are in early-stage discussions about a possible combination, with the deal’s strategic logic implying a combined entity with more than $12 billion in revenue across radio, satellite, and podcasting.

Within hours, the New York Times framed the talks as SiriusXM in early-stage discussions to acquire iHeartMedia. Variety described the same conversations as “early merger talks” being advised by Irving Azoff and Apollo Global Management. The Hollywood Reporter flagged a possible regulatory question through the podcast market, given SiriusXM’s lead in U.S. podcasting and iHeart’s position as a top-three publisher. TheWrap reported that Azoff was personally negotiating to purchase both entities and merge them, a framing The Desk explicitly noted has not been independently verified.

What’s consistent across the reporting: talks are preliminary, both companies declined to comment, and Apollo or another equity sponsor is functionally necessary to absorb iHeart’s roughly $5 billion debt stack without breaching SiriusXM’s covenant ceiling. What’s inconsistent: whether this is a sale, a merger of equals, or a third-party acquisition by an Azoff-led vehicle. Wall Street’s instant verdict (IHRT shares jumping approximately 35%, SIRI shares falling approximately 5%) priced iHeart as the rescued party and SiriusXM as the entity assuming the risk, per Deadline.

The Strongest Objections To The Deal

The most defensible arguments against this deal, the ones most worth taking seriously regardless of how often they’re being quoted in the trade press, lie at the intersection of three concerns.

The first is concentration in audio advertising. SiriusXM and iHeart are by many accounts the two largest podcast publishers in the United States by audience reach. Combining them with the largest AM/FM operator and the largest satellite radio service produces a single entity with the most addressable U.S. audio advertising footprint by a wide margin. The Hollywood Reporter explicitly flagged this as the cleanest antitrust question, and the relevant question has shifted in the years since the 2008 DOJ Sirius/XM closing statement from satellite-radio competition to podcast and audio-advertising concentration. RadioInsight’s analysis of the deal puts the asset map plainly: the combined entity would own the largest podcast network by reach, the largest audio syndication service (Premiere Networks), a leading audio rep firm (Katz), the exclusive YouTube audio advertising sales partnership, and multiple major streaming apps with both paid and ad-supported tiers.

The second is operational. SiriusXM’s CEO Jennifer Witz publicly described the company’s new $7 ad-supported and $9.99 music-only tiers as competing “squarely off against AM/FM listening” earlier this year. In other words, SiriusXM’s own management has been positioning the company against terrestrial radio at the exact moment it may end up acquiring 860 terrestrial radio stations. Radio Ink flagged this on April 24, and it remains the trade press’s sharpest single-paragraph observation about the deal: there is a genuine internal contradiction between SiriusXM’s recent strategic positioning and the implications of an iHeart acquisition.

I think this is actually the weakest of the three objections, because it assumes inaction. SiriusXM is full of very smart people. The premise that they would radically restructure their company by acquiring 860 broadcast licenses while leaving their consumer marketing and tier positioning untouched is doing a lot of work. One assumes that an organization willing to absorb $5 billion of iHeart debt has also thought through how it would reposition the $7 ad-supported and $9.99 music-only tiers against the new combined portfolio. The contradiction is real today. It would not survive day one of a closed transaction.

The third is local broadcasting. This is the framing that has dominated the LinkedIn conversation, and the one I want to engage with most directly. The argument runs roughly as follows: SiriusXM, having paid for 860 broadcast licenses, will treat those licenses as either simulcast surfaces for premium satellite content (the “frequency-based billboards” scenario), or as candidates for divestiture and closure in unviable markets, or as marketing top-of-funnel for paid subscriptions. In any of these scenarios, the localism remaining on those stations (local DJs, local newsrooms, local sports, local advertising relationships) is at risk. The cluster’s social and civic value to the markets it serves diminishes or disappears.

That third concern is the one I want to engage with most directly. The structural and financial objections will get settled by mechanical processes: whether Apollo writes a check large enough to retire iHeart’s high-yield paper at close, and whatever consumer-facing repositioning the combined company announces. The financial mechanics will be visible eventually in HSR filings and credit-facility waiver requests. (My understanding of those terms, by the way, I owe to Dr. Sheldon Balbirer, who taught me corporate finance in my MBA program. Shelly passed earlier this year. He would no doubt wince at my financial coverage, but my coverage is certainly better for the chance I had to study with him.)

The local-broadcasting concern doesn’t resolve that way. It depends on an empirical question that observers raising it tend to skip: how much localism is actually still on these stations to be lost? The answer to that question materially changes the analysis. And (in case we have forgotten), a local radio license carries a clear obligation, courtesy of the FCC, to “serve the public interest with programming responsive to the local community of license.”

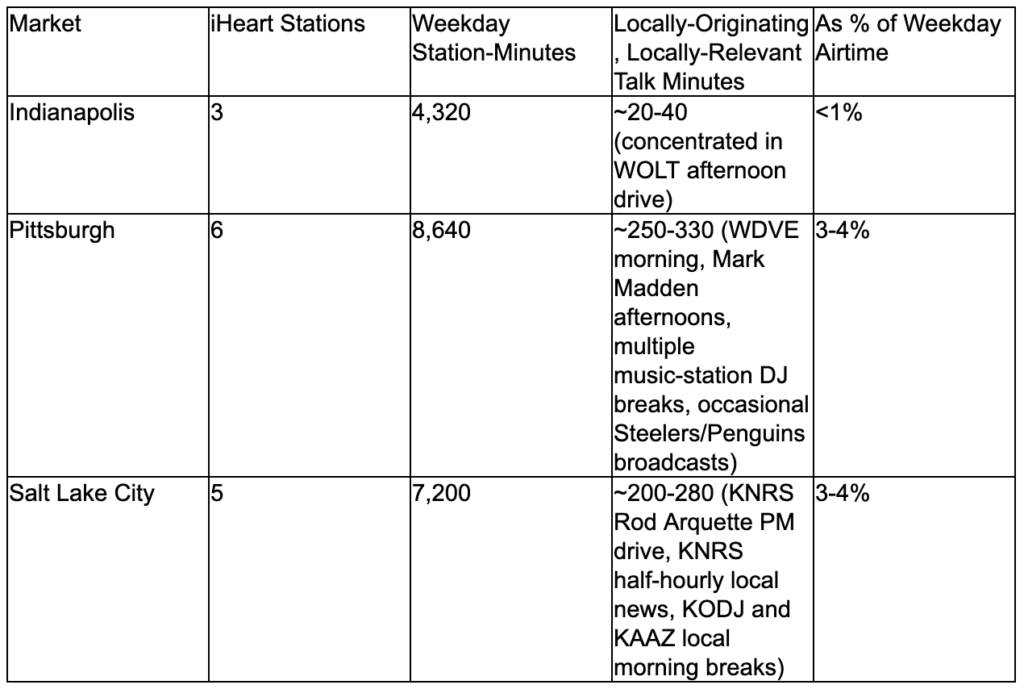

I spent some time this past week running a programming audit on iHeart’s clusters in three mid-size U.S. markets: Indianapolis, Pittsburgh, and Salt Lake City. The result is presented below in some detail because the empirical record matters here more than the rhetorical framing. What I found was consistent across all three markets and aligned with patterns documented in the radio trade press for at least 15 years. The summary, in advance: the localism that observers fear losing has, with limited and specific exceptions, already been gone for some time.

What’s “Local”: A Three-Market Audit

I selected three U.S. markets for this audit using two criteria. First, mid-size: large enough that you would expect significant local programming if any was going to exist, and small enough to avoid the markets that are themselves origination points for nationally syndicated iHeart content (New York, Los Angeles, Chicago, Nashville, Atlanta, Phoenix). Second, geographic and cultural diversity: Midwest (Indianapolis), Northeast Rust Belt (Pittsburgh), and Mountain West (Salt Lake City).

What follows is each cluster station-by-station, with the principal weekday programming as of late April 2026.

Indianapolis (DMA 25)

iHeart’s Indianapolis cluster comprises three stations.

WFBQ 94.7 FM, “Q95” (classic rock). The morning daypart is The Bob & Tom Show, weekdays 5 a.m. to 10 a.m. Eastern. The show originates from WFBQ’s studios, but it isn’t “Indy’s Morning Zoo.” It’s a national comedy program built around touring comedians dropping by to do bits and pre-produced parody segments. It could originate from Alaska, and it wouldn’t change the show one whit. It has been syndicated nationally by Cumulus Media, iHeart’s competitor, since 2014. Bob Kevoian, the show’s co-namesake, retired from on-air duties at the end of 2015 and died on April 17, 2026, at 75, after a three-year stomach cancer fight. Tom Griswold continues to host with Kristi Lee, Chick McGee, and others.

I should note here that I worked with the show some years ago, doing some research at their home base in Indianapolis. The thing I remember most about both Bob and Tom is how lovely they were to work with. Their gift was the discipline the best comedy hosts have: stepping back and letting the guests do the funny thing. Elvis Duran has that same skill, by the way, and Elvis is iHeart’s; he’s maybe the best traffic director in radio. The Bob & Tom Show has been the home of American comedy for the better part of forty years. Bob will be missed.

After the morning block, Q95’s programming is voice-tracked midday talent of unknown origin, and a syndicated Nights with Alice Cooper that originates from Phoenix.

WNDE 1260 AM, “Fox Sports 1260” (sports talk). Effectively the Fox Sports Radio national feed, broken only by occasional Indianapolis Indians (Triple-A baseball) play-by-play. The full weekday lineup as of this writing: Ben Maller (overnight), Two Pros and a Cup of Joe (6-9 a.m. ET), The Dan Patrick Show (9 a.m.-12 p.m. ET), The Herd with Colin Cowherd (12-3 p.m.), The Doug Gottlieb Show (3-5 p.m.), Covino & Rich (5-7 p.m.), The Odd Couple (7-10 p.m.), Jason Smith (10 p.m.-2 a.m.). All syndicated.

WOLT 103.3 FM, “Indy 103.3” (alternative rock). Format-flipped to “alternative from the 90s and 2000s” in August 2022. Mornings: The Woody Show, syndicated from KYSR Los Angeles. Middays: voice-tracked by an out-of-state announcer. Afternoon drive: a local host named Ben, the one daypart on the station that originates in Indianapolis. Evenings: a syndicated host. Outside of afternoons, all DJ shifts are syndicated from out of state.

Pittsburgh (DMA 23)

iHeart’s Pittsburgh cluster is the largest of the three I audited, with six stations.

WDVE 102.5 FM (classic rock; Pittsburgh Steelers radio flagship). Morning drive: Randy Baumann & The DVE Morning Show, local. Afternoon drive: post-Sean McDowell’s 2019 retirement, the lineup mix is unclear in the available reporting. Steelers play-by-play and select sports calls from Mark Madden contribute additional local content during football season.

WBGG 970 AM, “Fox Sports 970” (sports talk; Steelers/Penguins co-flagship). Predominantly the Fox Sports Radio national feed, similar to WNDE Indianapolis, with carve-outs for Pittsburgh Steelers and Pittsburgh Penguins broadcasts and Robert Morris University football, men’s basketball, and men’s ice hockey. Historically, WBGG carried local hosts including Tunch Ilkin (deceased 2021) and Stan Savran (deceased 2024); the current local lineup outside of game broadcasts is significantly thinner than it was a decade ago.

WPGB 104.7 FM, “Big 104.7” (country). Overnights: After MidNite with Granger Smith (syndicated from iHeart’s WSIX Nashville). Mornings: The Bobby Bones Show (also syndicated from iHeart’s WSIX Nashville). Middays: Angie Ward (voice-tracked from iHeart’s WUBL Atlanta). Afternoon drive: Kasper, local. Evenings: Travis, local. Roughly 8 hours of local airtime per weekday against 16 hours of syndicated or voice-tracked content.

WWSW 94.5 FM, “3WS” (classic hits). The most locally-staffed station in the cluster: Jonny Hartwell and Val Porter handle weekday mornings 5-10 a.m., Tall Cathy handles middays 10-2, and Mike Frazer handles afternoon drive 2-8. Five live local airstaffers, plus weekend and fill-in coverage from program director David Edgar. Out-of-town voice-trackers and syndication on overnights and weekends.

WKST 96.1 FM, “Kiss FM” (Top 40). The Kiss Morning Freak Show in mornings (with named talent including Tall Cathy, who also works WWSW middays). On Air with Ryan Seacrest in the evening daypart, syndicated from iHeart’s KIIS-FM Los Angeles. Most other dayparts are voice-tracked or syndicated.

WXDX 105.9 FM, “The X” (alternative rock). Morning drive: The Woody Show, syndicated from KYSR Los Angeles. Middays 10 a.m.-1 p.m.: Abby Krizner (program director), local. 1-3 p.m.: Travis (also evenings on WPGB), local. 3-7 p.m.: Mark Madden afternoon sports talk on an alternative rock station, a Pittsburgh-specific choice that reflects the market’s appetite for local sports-talk content. Worth noting: The Woody Show in Pittsburgh is the same Woody Show that wakes up Indianapolis on WOLT, broadcast from the same Los Angeles studios. One morning show, two “local” identities.

Salt Lake City (DMA 28)

iHeart’s Salt Lake City cluster comprises five active stations after the company surrendered KWDZ’s license in 2018.

KNRS 570 AM / 105.9 FM, “Talk Radio 105.9” (news/talk). The flagship for nationally syndicated political and consumer talk: Glenn Beck, Sean Hannity, The Clay Travis and Buck Sexton Show, Jesse Kelly, Dave Ramsey, and Coast to Coast AM with George Noory. The single local daypart is Rod Arquette in afternoon drive. The station reports a full news department with local news every thirty minutes weekdays.

KODJ 94.1 FM, “Utah’s Greatest Hits” (classic hits). Mornings 6-10 a.m.: Meredith & AJ, local husband-and-wife team. Other dayparts feature The Martha Quinn Show (syndicated through iHeart’s classic hits network) and additional named talent whose live-versus-voice-tracked status I was unable to confirm.

KJMY 99.5 FM, “My 99.5” (hot adult contemporary). Mornings: Valentine in the Morning, syndicated from KBIG Los Angeles. Evenings 5-9 p.m.: Toby Knapp, syndicated from WIHT Washington, D.C. The station is essentially all-imported.

KZHT 97.1 FM, “97.1 ZHT” (Top 40). Mornings: The Fred Show, syndicated from WKSC Chicago since January 2025. American Top 40 is syndicated weekly. The Top 40 station is essentially all-syndicated from iHeart properties in other cities.

KAAZ-FM 106.7 FM, “Rock 106.7.” Mornings: Hooker & DB, local. Other dayparts not fully detailed in the available reporting; the format suggests significant voice-tracking outside the morning drive.

Cross-Market Pattern

I want to be precise here about what I’m counting and what I’m not, because there’s a generous version of this analysis and a strict one, and only the strict one is honest.

What I’m counting as “locally-originating, locally-relevant” content is the actual minutes per weekday when a person broadcasting from a studio in that market is speaking content that addresses or connects to that market specifically. What I’m not counting: music (Sabrina Carpenter and the Rolling Stones aren’t local content); syndicated programming, even when it originates locally but addresses a national audience (Bob & Tom is produced in Indianapolis but the content is national in flavor: touring comedians and pre-produced parody bits, not the city it broadcasts from); voice-tracked imports from out of market; advertising of any kind (a separate category I’ll address below); and station-branded production elements that play identically across iHeart properties. A three-hour DJ shift on a music station might contain four to six minutes of actual DJ talk per hour. The rest are songs and spots. I’m counting the four to six minutes, not the three hours.

Pittsburgh is the local-content outlier of the three by a comfortable margin, pulled up by genuine sports-talk content on WXDX and the depth of local talent at WDVE. Even there, fewer than 4% of weekday airtime minutes feature a person broadcasting from Pittsburgh about Pittsburgh. Indianapolis is effectively zero. The five-hour morning show that anchors the cluster originates in Indianapolis but doesn’t address it. Salt Lake City sits between the two, pulled up by the KNRS news/talk format and its half-hourly local newscast cycle.

It’s also worth being precise about what that locally-originating content actually is, because not all locally-originating content is created equal. In Pittsburgh, where the percentage is highest, the dominant local content is Steelers and Penguins play-by-play, Robert Morris University game broadcasts, and Mark Madden’s afternoon sports talk. The rest is DJ banter between songs on music stations. In Indianapolis, the local content is afternoon-drive DJ banter on a music station, plus occasional Indianapolis Indians broadcasts. Only Salt Lake City’s KNRS, with Rod Arquette’s afternoon show and a half-hourly local news cycle, carries any meaningful amount of local talk and news.

Across all three markets, the locally-originating content that survives is heavily skewed toward sports and song intros, with a thin layer of local news and talk on a single station in one market. That’s a real category, and it has real economic and cultural value. But it isn’t what most observers mean when they worry about losing local radio.

If Pittsburgh, a market with a genuine local-radio culture, strong sports-team anchoring, and the most-staffed iHeart cluster of the three, looks like this, the smaller markets in iHeart’s footprint look measurably worse.

This pattern is not new. The Indianapolis Business Journal documented it in a 2011 piece titled “Music stations doing just fine without on-air DJs.” The article noted that WFBQ’s then-midday host, Laura Steele, was simultaneously voice-tracking shows in Dallas, San Antonio, and Seattle, pretending to be local in four cities at once. That was fifteen years ago. The model has only intensified in the years since.

It’s also worth noting that iHeart’s footprint has been contracting in some markets for some time, in some cases predating the current company structure. Kansas City is one such example: iHeart’s predecessor, the Jacor/Clear Channel combination, swapped out of Kansas City in 1997, and the market is currently operated by Audacy and Cumulus Media. Audacy alone runs eight stations across six formats there. (Kansas City Radio History traces the post-Jacor ownership chain through Bonneville, Entercom, and into the present-day cluster.) This isn’t a hypothetical scenario about what could happen to iHeart’s stations in a SiriusXM transaction. It’s a documented precedent for divestiture in a market the company’s predecessor once operated in.

What “Local Content” Actually Means On Commercial Radio

I worked on a significant content analysis project for the FCC about twenty years ago, and one of the findings I’ve kept thinking about for two decades is this: the most legitimately local content on the average commercial radio station, by airtime minutes, is the local advertising load. Not the DJ talk, which on most stations is dominated by backsell, cross-promotion, and station-branded bits that could play in any market. Not the music, which is sourced from the same record labels as every other station in the format, and largely no longer informed by local research (certainly the case for iHeart). Not the news, which has progressively shifted from originated reporting to stringer-read network feeds. The local plumber’s spot. The personal injury attorney. The regional Honda dealer. The heating-and-cooling company that has been running the same tag line for fifteen years. Those advertisements, with their local phone numbers and local addresses and local references, constitute the bulk of what a typical commercial radio station broadcasts that is genuinely local in any meaningful sense.

This finding tends to be uncomfortable for radio’s defenders, because it relocates the case for local broadcasting from cultural infrastructure to commercial infrastructure. But it’s the empirically supported claim. Across the three iHeart clusters audited above (fourteen stations, 20,160 station-minutes of programming per weekday), the locally-originating, locally-relevant on-air talk content totals roughly 560 minutes by my estimate, or about 2.8% of weekday airtime. Most of that comes from one or two local talkers per market. The local advertising load, by contrast, runs in the range of 8-15 minutes per hour across most dayparts on most stations. Even on a generous assumption that only half that inventory is sold to local or regional accounts, the actually-local commercial content on these stations exceeds the actually-local talk content by a factor of three or four to one.

If observers want to mourn what’s at risk in a SiriusXM acquisition of iHeart, this is the thing actually at risk: not the local DJ (there are very few of them left to lose), but the local advertising layer. That’s the only place these stations carry significant local commercial texture, and it’s the place where a buyer’s plans matter most.

What SiriusXM Brings

The 860 stations are inventory: transmitter networks with audiences attached. They are not, in any meaningful sense, content. The content has been gone for twenty years. iHeart is genuinely a content company in many segments. Its podcast network grew 24.5% in Q4 2025 to $564 million in podcast revenue for the full year, its digital audio segment grew 14.2% in 2025, and its syndication arm, Premiere Networks, remains a substantial talent pool. The talent and content business is real. But the 860 transmitters have been carrying other people’s programming for a long time.

SiriusXM, by contrast, has built a portfolio of audio properties that consumers pay to hear. The satellite operation reported 31.3 million self-pay subscribers and $15.11 ARPU at year-end 2025, against $1.26 billion in free cash flow (up 24% from the prior year) with FY2026 guidance of approximately $1.35 billion. The company’s podcast operation grew 41% in 2025. SiriusXM has also built a formidable sales operation, both through key acquisitions (Pandora and AdsWizz among them) and by attracting top sales talent away from other companies, including some of broadcast radio’s best sellers. And in 2026, SiriusXM became YouTube’s exclusive audio advertising sales partner, not a small thing given that YouTube is now the largest single destination for podcast consumption in the United States.

This portfolio matters specifically because of what’s at stake. If the local advertising layer is the actual asset being bought along with iHeart’s transmitters, then the relevant question is whether a SiriusXM-led organization handles that layer better or worse than iHeart has. iHeart’s commercial radio sales operation has been operating under significant constraints. The company carried just over $5 billion in total debt at the end of 2025, with $440 million in annual interest expense, which consumed roughly 64% of its $686 million in Adjusted EBITDA. Layoffs, cost cuts, and sales-force attrition have been documented across the trade press for several years.

None of which, to be very clear, is the fault of the iHeart employees at those local stations. They’ve continued to do sterling service, keeping those properties going, in some cases burning the metaphorical furniture to keep warm, to pay for the sins of Clear Channel’s over-leveraging years ago. The constraint is structural, not individual. The people running these stations are doing the same job they’ve always done, with fewer resources and tighter margins.

The argument that SiriusXM’s better-resourced sales infrastructure could improve, rather than diminish, the local-advertiser-facing business is empirically defensible. It is not a foregone conclusion. But it’s a real possibility, and most of the LinkedIn discourse over the past week hasn’t entertained it.

Three Real Risks

I’d be making a different mistake if I walked away from this thinking the deal has no real-world stakes for the markets these stations serve. It does. The local advertising layer is real, and it would be naive to assume any acquirer’s incentives are perfectly aligned with preserving it. Three scenarios are particularly worth watching.

The first is the conversion of iHeart’s broadcast inventory into simulcast surfaces for SiriusXM premium content, the “frequency-based billboards” scenario referenced in some of the analytical commentary on the deal. Under this approach, stations remain on the air but with effectively zero locally-originated programming, and the local advertising layer becomes ancillary to a paid-subscription marketing strategy. This would significantly compress the local commercial layer.

The second is the consolidation of iHeart’s local sales operations into the combined company’s national ad-sales infrastructure. National-scale audio advertising operates on different unit economics than selling local accounts on local stations. If SiriusXM treats the local sales operation as an integration target rather than a distinct line of business, the local component disappears even if the transmitters keep broadcasting.

The third is asset-level divestiture or closure in unviable markets. iHeart has already done this. The Kansas City exit referenced above is the cleanest example. SiriusXM may follow a similar pattern in markets where the cluster economics no longer work, particularly given the change-of-control redemption provisions on iHeart’s 2029-2031 notes that would force any acquirer to retire roughly $5 billion at par regardless of secondary-market discounts.

These are all real risks. None of them is the same as “SiriusXM will kill local radio,” because the local radio being mourned was already largely gone. But they are honest concerns about the local advertising layer, the local sales operation, and the markets where these stations still play meaningful commercial roles. They deserve more attention than they have received, and the framing that has dominated the trade press has been pulling the conversation away from them.

A Closing Thought

What I want to leave readers with is not a prediction about whether this deal happens or what it will look like if it does. Those questions will be resolved in HSR filings, credit-facility waivers, and earnings calls. What I want to leave readers with is a recalibration of the framing.

The reporting and the trade-press conversation around this deal have proceeded as though SiriusXM is potentially acquiring 860 working community institutions whose localism is what makes them valuable and what makes the acquisition socially consequential. The empirical reality, based on the programming actually airing on these stations in late April 2026, is that the localism left to lose is small, concentrated in specific dayparts on specific stations in specific markets, and overwhelmingly secondary to a wall of national syndication and voice-tracked imports.

The localism that remains in commercial value, if not in cultural visibility, is the local advertising load, which is precisely the layer that makes the relevant question about a SiriusXM acquisition not “will they kill local radio” but rather would the combined entity actually serve those local markets better than iHeart did.

I think they could. I’m not certain. But I think it’s the more interesting question to ask, and it deserves more attention than it has received in the trade press over the past week.